Money Is Earned. Freedom Is Built.

A citizen who cannot fund his own life will eventually accept any terms — which is why financial literacy is not a math elective. It is liberty's economic leg. This campus teaches the whole of it, by doing: earning, budgeting, banking, credit, investing, taxes, protection, and the first business. Free, forever.

The 50/30/20 rule — the first budget every family can run this month.

Start the Seven Pillars ↓The Seven Pillars of Financial Literacy.

Everything a young person needs to reach economic independence, in the order it's needed. Nothing theoretical, nothing skipped.

Earning & Budgeting

Money is earned — that's lesson one, and everything stands on it. Build and balance a real budget, track every dollar, master needs versus wants, and run the 50/30/20 rule as a family.

Banking & Managing Money

Accounts, deposits, debit cards used safely, and the paper skills nobody teaches anymore — plus custodial accounts (UGMA/UTMA): the legal machinery families use to put real investments in a child's name.

Debt & the Credit Score

How interest and amortization really work — and the two honest schools of debt: the manage-it school (build the score, use credit strategically) and the avoid-it school (behavior beats math; remove the temptation entirely). We teach both at full strength. Your family decides.

Saving & Investing

Compound interest — the eighth wonder, demonstrated with your child's own numbers. Stock-market basics, long-horizon goals, and why time in beats timing.

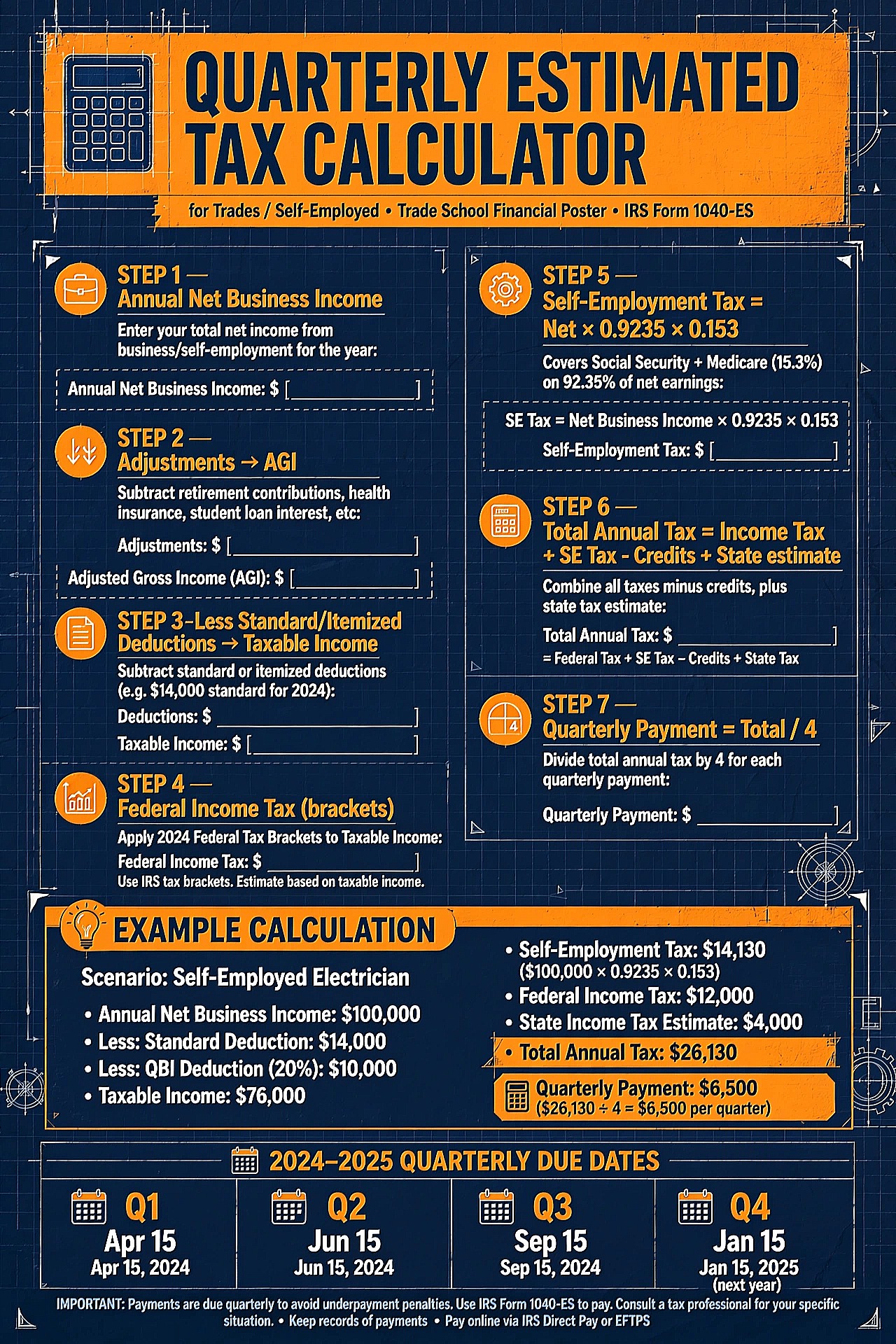

Taxes & the Civic Ledger

Income tax, sales tax, property tax: how each works, what each funds, and how to read a paycheck stub without flinching. The citizen who reads the ledger audits the government.

Protecting Wealth

The emergency fund — the wall between a bad week and a bad decade — and insurance decoded: health, auto, home; what each number on the policy means before you need it.

The First Business

Lemonade stands, lawn jobs, babysitting ledgers: profit, loss, pricing, and the day a young person discovers they can create income instead of only receiving it.

The Goal: Economic Independence

Not riches — independence: the state in which no one can buy your compliance, because your life is funded by your own competence. That is the pillar the other seven hold up.

The Map Nobody Hands Parents.

Serious free finance education already exists — built by institutions with no upsell — but it's scattered. Here is the honest map. None of these are GSU products; all are free and worth your family's time.

The IRS's Own Curriculum

Understanding Taxes — twelve free modules from the source itself: the Hows (W-2s, withholding, deductions, credits, filing) and the Whys (progressive vs. regressive vs. flat, and what taxes fund). Understanding Taxes →

The Federal Consumer Lab

The Consumer Financial Protection Bureau publishes free budgeting simulations and youth money activities — including 50/30/20 exercises with real household profiles. CFPB Youth Education →

The GSU Knowledge Layer

Our free games drill the concepts under all of it — budgeting, compound interest, credit, the paycheck — taught by doing, with consequences. The Library →

The Map to Independence.

FREEDOM: The Definitive Guide to Financial Independence

Liberty's economic leg, mapped end to end: the escape route from dependence, the building of self-funded life, and the discipline that no windfall can substitute. The complete adult companion to everything on this page.

The Money Games.

Teach-then-play, infinite, and free — arithmetic with consequences, the way money actually teaches.

Already on the Shelves

Finance and wealth games live in the Library today — play free, no account required. Enter the Library →

The Budget BuilderComing Soon

Run a household month by month — then the wheel spins: job loss, medical bill, car trouble. Keep the 50/30/20 line through the shocks, or learn exactly why the emergency fund exists. Optimism bias, cured by play.

The Compound ClimbComing Soon

Watch the eighth wonder work: start early or start late, and race the curve that decides retirements.

The Credit TrapComing Soon

Minimum payments, teaser rates, and the long arithmetic of interest in reverse — escape the maze or map why you couldn't.

The Paycheck DecoderComing Soon

Gross to net, line by line: withholding, the taxes, the deductions — read the stub like an adult.

The Lemonade LedgerComing Soon

Price the cup, count the costs, survive the slow Saturday: profit and loss as a first business teaches it.

The Lease ReaderComing Soon

Three of four renters sign without reading. Dissect the lease, find the trap clauses, negotiate the terms — before the signature, not after.

The Financification Comprehension Certification Launches July 4, 2026.

Free, anonymous, serial-numbered, publicly verifiable — economic independence begins with demonstrated understanding. The date is not a coincidence.

See Every Certification →

GENO AI Tutor available 24/7 — a robot you can actually TALK to.

Ask him to run the compound-interest math on your child's actual allowance, explain a credit score, or decode a paycheck stub line by line — out loud, in 32 languages, free, from the corner of every page on this site.

Financification FAQ

What is the 50/30/20 rule?

The simplest working budget: 50% of after-tax income to needs (housing, food, utilities, transport), 30% to wants, and 20% to the future (savings, investing, debt paydown). It's not the only budget — it's the first one, because a family can start it this month and adjust from experience.

What age should financial education start?

The moment a child can count coins. Early years: earning, saving jars, needs versus wants. Middle years: budgeting, banking, and the first compound-interest demonstration with their own numbers. Teen years: credit, taxes, paychecks, insurance, and the first business. The sequence on this page runs in that order on purpose.

Why does compound interest matter so much?

Because it works in both directions and rewards time above all. Money invested early multiplies across decades; debt carried at interest does the same in reverse. A teenager who truly understands the curve — by running their own numbers — makes different decisions at twenty than one who memorized the formula.

Is everything here really free?

Yes — the curriculum, the games, and GENO tutoring are free forever with no account required. GSU is run by The Foundation for Global Instruction, a 501(c)(3) nonprofit. The companion book FREEDOM is available for families who want the complete deep-dive, but the campus costs nothing.

Should my child learn to use credit cards, or avoid debt entirely?

The finance-education world splits into two honest schools: the pragmatic school teaches that credit is unavoidable, so build the score and use it strategically; the behavioral school teaches that human behavior beats math, so remove consumer debt entirely. Both have produced financially free adults. We present both at full strength — the same both-lenses standard we apply to every contested question — and trust your family to decide.

What are UGMA and UTMA custodial accounts?

Legal frameworks that let a family put real investments in a child's name: the gift is irrevocable (it becomes the child's property), a custodian manages it until the age of majority, earnings face capital-gains tax, and — the trade-off families must weigh — student-owned assets count heavily against needs-based college aid. A live lesson in finance and law at once.

Is this financial advice?

No — it is financial education: the concepts, the math, and the vocabulary of economic independence. For decisions about your specific investments, taxes, or insurance, consult a licensed professional. Our job is to make sure you understand every word they say.